Healthcare risk is mispriced in different ways depending on who's doing the pricing. In some cases, nobody's pricing the risk at all.

PBMs pass pharmacy costs through to employers without guarantees and the employer absorbs all the volatility, while the PBM keeps the spread between what it charges and what it pays. Carriers and health plans price at the group or demographic level when actual risk varies by individual member, drug, or physician. Actuarial benchmarks from consulting firms like Milliman ($1B+ annual rev) lag reality by 12–18 months. ACOs and provider groups are taking downside risk with little actuarial infrastructure, yet make million-dollar decisions based on simple spreadsheet analyses.

The opportunity for better underwriting differs in each case: make hidden costs visible, price at the right resolution, bring more real-time data, or introduce risk pricing where none exists.

This gap is not just because incumbents can't build the technology, but because they are not incentivized to do so. PBMs have the data to price at the drug level but won't because the spread between what they charge plan sponsors and what they pay pharmacies is their margin, and transparent pricing would eliminate it. Carriers could price at the individual level, but their entire regulatory and capital structure (reserve calculations, community rating, MLR floors, reinsurance) is built around group-level pooling. ACOs and provider groups are clinically-focused organizations being asked to bear complicated financial and actuarial risk without the required tools or infrastructure.

Why now: tailwinds are converging to make this investable at scale

Historically, healthcare cost reduction has focused on shaving costs around the edges of an inflated incumbent price using “back-end optimization” (step edits, care management, site of care optimization, utilization review, prior authorization, etc). We've reached an inflection point where that's not enough.

Employer healthcare costs are rising at the fastest rate in 15 years. Projections for 2026 range from 9% to 10%, pushing average costs above $18,500 per employee (62% higher than 2017). The pool of risk-bearing entities keeps expanding (67% of covered workers now in self-funded plans, 477 MSSP ACOs managing 11.2M beneficiaries) but most lack actuarial infrastructure.

On the policy side, CMS is compressing the timeline for ACOs to take downside risk as the CY 2026 PFS final rule caps one-sided risk at five years, down from seven originally. H.R. 1 cuts federal Medicaid funding by ~$900B over 10 years (7.5M projected to lose coverage), which shifts cost and acuity risk onto commercial populations. MA reported its first collective underwriting loss in 2024 (89.9% loss ratio), forcing ~3M beneficiaries to find new plans.

All of these trends create new buyer segments that need underwriting infrastructure they don't have.

Startups can exploit this by pricing precisely, or by introducing guarantees where none exist

Instead of cost optimization at the edges, the new model we're seeing in some pockets replaces the price entirely: guarantee a lower number upfront, bear the risk, and capture the spread.

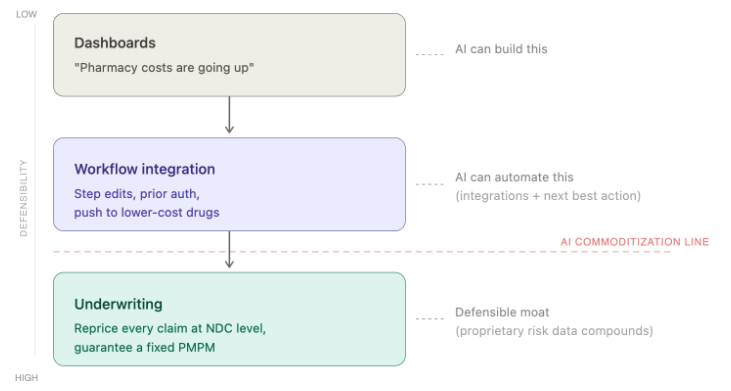

To be clear, when we talk about underwriting and taking risk, it's much more than a VBC model with shared savings or downside risk for a primary care group. We're taking a broader view of "pricing risk" here. Pharmacy is a useful example because PBMs have no risk infrastructure today. Consider the three basic layers:

Layer 1 - Dashboards/Analytics. Dashboards to upload claims, show trend, and run cost analyses.

Layer 2 - Workflow Integration. Step edits, formulary design, prior authorization, patient steerage. This is where you touch the operation and earn the data. Valuable, but increasingly commoditized by AI.

Layer 3 - Underwriting. Guarantee a number — a fixed PMPM, a shared savings rate, a bundled episode price — and bear the risk.

Dashboards and workflow tools are getting cheaper to build and easier to replicate, which compresses the value of Layers 1 and 2 and pushes margin toward Layer 3. The underwriting layer can't be commoditized because it requires proprietary data, actuarial precision, and the willingness to stand behind your math.

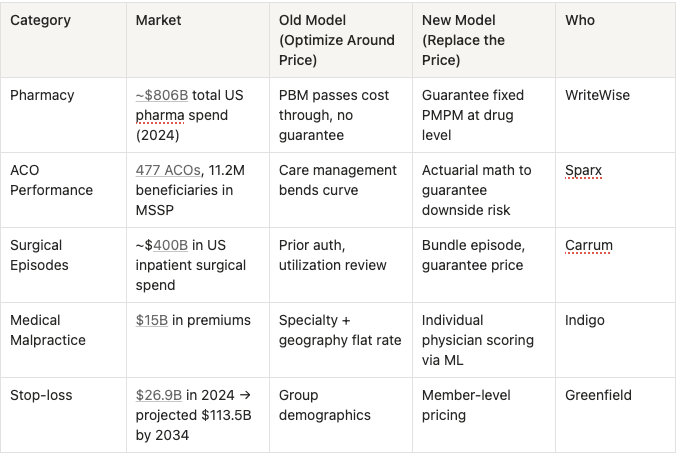

The pattern repeats across verticals:

In our portfolio, WriteWise reprices pharmacy claims at the individual drug level and guarantees employers a fixed PMPM. To do so, they assembled data that PBMs won't share with each other and no single market participant can replicate. Outside the portfolio, Sparx underwrites ACO risk and has unlocked $1B+ in reinsurance capacity by giving ACOs the actuarial confidence to take downside contracts. Indigo now auto-underwrites 20% of malpractice submissions through its proprietary AI platform, Lux, pre-scoring every US physician individually compared to legacy carriers pricing all OBs in Florida at ~$120K/year regardless of history.

The edge at these companies isn't an AI breakthrough. It's clever actuarial work, data aggregation earned through GTM focus, and doing things incumbents are structurally unable to do.

The moats compound

What makes this a compounding advantage rather than a one-time arbitrage is the flywheel between data and capacity:

- Data: Every claim and outcome feeds the pricing model. WriteWise gets more precise with every employer group. Sparx improves with every ACO performance year. No new entrant can replicate years of claims history on day one.

- Capacity: Operational execution produces the outcomes the model predicted, which validates the model, which earns reinsurance capacity, which lets you take on more risk.

Critically, operational execution is the underwriting edge. You can't just price risk but you have to deliver on the guarantee. WriteWise routes patients to lower-net-cost drugs Carrum redirects up to 30% of members initially recommended for surgery to less invasive treatment options and reduces readmissions by up to 80% relative to the national average. .

The clinical operation reduces variance, which tightens the guarantee, which earns more capacity. Companies that take risk but can't execute operationally blow up on loss ratios.

We'd love to chat with founders building these types of underwriting platforms or using this underwriting lens to re-wire financial flows in healthcare.

Additional Reading:

- MedPAC, "The Medicare Advantage Program: Status Report" (Mar. 2025)

- SOA Research Institute, "Evaluating Risk Adjustment and Medicare Advantage" (Feb. 2025)

- Swiss Re, "An Expanded Role for AI in Life & Health Predictive Underwriting" (Feb. 2025)

- Milliman, "Under Pressure: ACPT Pushing Down on 2024 and 2025 MSSP Starters" (Nov. 2025)

- Health Affairs Forefront, "Medicare ACOs In 2024: Increased Participation and Evolving Policy Impacts" (Nov. 2025)

- SOA, "Reimagining Pharmacy Financing in the Commercial Space Using a Value-Based Reimbursement Model"

- Penn LDI / Health Affairs, "Future Bundled Payment Models Need To Engage Physician Group Practices" (Apr. 2024)

- PwC Health Research Institute, "Medical Cost Trend: Behind the Numbers 2026"

- DOL / Federal Register, "Improving Transparency Into Pharmacy Benefit Manager Fee Disclosure" (Jan. 2026)

- Drug Topics / PSG, "PBM Unbundling: New Pricing Models Create More Transparency" (Jan. 2026)

- Paragon Institute, "Two Paths for Medicare's Future: Medicare Advantage and ACOs" (Jan. 2025)

- Fierce Healthcare, "2026 Outlook: The Domino Effect of Medicaid Cuts" (2026)

- MedPAC, "Payment Basics: Accountable Care Organizations" (2025)