Overview

For 20+ years, policymakers have been handing Americans the keys to their own healthcare spending. Every year, billions of dollars earmarked for care sit untouched not because Americans don't need it, but because the infrastructure to spend it was never built.

Employers are shifting from defined-benefit (“we choose your plan and pay claims”) to defined-contribution (“here's a budget on a card, go buy what you need”). HSA assets hit $159B across 40M accounts growing 16% YoY. ICHRA enrollment tripled in 2026 with 92% employer retention. The OBBBA (signed July 2025) reclassified all Bronze and Catastrophic ACA plans as HSA-eligible and made DPC memberships payable from HSAs for the first time. This growth is the largest single-year expansion of consumer-directed healthcare eligibility in history with roughly 25M+ additional Americans now in HSA eligible health plans. At the same time, employer healthcare costs are rising 9.5% in 2026 (highest in 15 years) and 59% of employers are making cost-cutting plan changes. This trend is driving HDHP enrollment from 27% to 33% of covered workers with 2/3 of new hires selecting consumer-directed health plans.

The shift is real, but 20+ years of evidence proves consumers won't simply become healthcare shoppers or consumers when funds are loaded on a card top-down from employers or TPAs they don’t engage with or know. 47% of privately insured adults with deductibles above $3,000 skip needed care because of cost. 51% of HSA accounts have balances under $500. Average HSA contributions are $791 against a $4,400 limit. 91% have zero invested assets. Only 36% of employees can even identify that their employer offers an HSA.

How can we expect consumers to “shop” for care if there’s a >50% chance the card will be denied at the point of sale?

This behavioral failure is not a bug but a structural opportunity for startups. The gap between "having an account" and "using it optimally" destroys $50-60B+ annually: FSA forfeitures, unrealized HSA tax savings, HDHP holders who never open an HSA, wrong plan selection, and foregone investment returns on uninvested balances. This is the same dynamic that made Fidelity, Vanguard, and Schwab trillion-dollar businesses. Those companies didn't win because 401(k) participants became savvy investors but because they built infrastructure (target-date funds, auto-enrollment, auto-escalation) that acted on behalf of participants who wouldn't act for themselves.

We think the same value migration is happening in healthcare: from account custodians (where the product is 90-95% commodity across the Big 4) to verification and routing infrastructure that closes the behavioral gap by acting for consumers.

Four tailwinds are widening this gap simultaneously:

- Prescriptions moving from claims rails to card rails, starting with GLP-1s. GLP-1 prices fell from $1,000+/month to $149-350 via oral Wegovy, TrumpRx, and manufacturer cuts. LillyDirect and NovoCare both accept HSA/FSA at checkout. GLP-1 spending is doubling annually, and 1-year persistence hit 62.6% (up from 33% in 2021) — these are recurring card transactions the existing substantiation infrastructure can't handle. This direct-to-patient trend will only continue in other therapeutic areas with >90% of pharma companies currently working on a direct-to-patient strategy.

- New consumer front doors are funneling demand to card-based purchases. Amazon's health AI agent serves 200M Prime members and accepts HSA/FSA everywhere. Function Health hit $100M ARR (450% YoY) accepting HSA/FSA. ChatGPT Health has 230M weekly health users but no HSA/FSA compliance layer on its Stripe checkout — the single largest infrastructure gap in consumer healthcare.

- OBBBA and employer cost pressure put ~25-27M additional Americans in HSA-eligible plans. OBBBA directly reclassified ~10-12M (Bronze/Catastrophic + off-exchange), while employer HDHP enrollment jumped from 27% to 33% of covered workers (~15.6M additional lives). Bronze selection rates surged nationally after enhanced subsidies expired resulting in higher premiums for many Americans. DPC memberships are now HSA-eligible at $150/month but DPC practices have no payment infrastructure for HSA verification, and the IRS left "primary care services" undefined.

- The verification infrastructure is collapsing. The workaround for verifying complex transactions is growing 10x while coming under regulatory scrutiny simultaneously. SIGIS, the only item-level eligibility protocol for HSA/FSA card transactions, is 20 years old, maintained as a CSV of products that retailers download monthly. 25-33% of non-pharmacy transactions still require manual review (Internal Analysis). Payment facilitators are routing non-medical merchants through medical MCC codes, and the IRS has flagged the process.

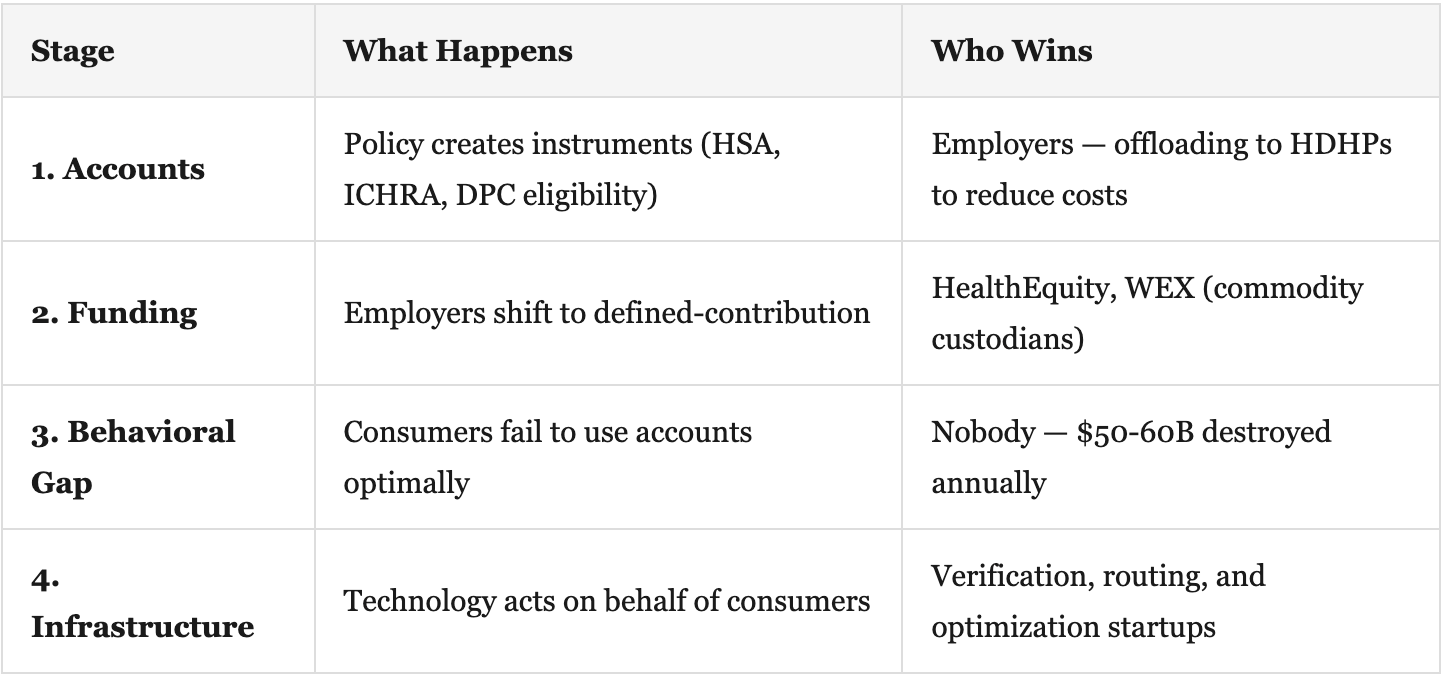

What This Means Going Forward

We think about the opportunity across a 4-stage lifecycle:

Verification is the wedge

When a consumer swipes an HSA card at a merchant, the issuing bank sees a 4-digit merchant category code and a dollar amount but not what was purchased or whether it's eligible. Every party in the payment chain needs independent verification: payment facilitators can't self-certify, TPAs bear IRS liability for FSA spend but receive no data from card networks, and card networks carry zero clinical data in the ISO 8583 authorization protocol.

We see this playing out across three near-term opportunities:

Neutral substantiation infrastructure. The ~300 consumer-directed health administrators who bear IRS liability for every unsubstantiated FSA dollar spend $2-5 per claim on manual review. A neutral third-party layer that ingests receipt data from payment facilitators and merchants, substantiates in real time, and returns a verified result to the TPA is infrastructure that every party needs. At scale, the analogy is SureScripts (30.5B transactions/year in e-prescribing), which is a neutral network that became un-displaceable because both sides needed it.

Multi-fund payment routing. Consumers carry 3-5 healthcare payment instruments (HSA, FSA, HRA, ICHRA, personal card) and don't know which to use at checkout. No infrastructure exists to split a single transaction across fund sources. Auth rates crash when benefit platforms attempt pre-tax migration because the routing logic doesn't exist. The infrastructure that automatically routes "this item from HSA, that item from HRA, remainder on personal card" removes a decision consumers will never make.

AI-to-commerce HSA/FSA rails. When ChatGPT Health recommends a supplement, lab test, or DPC visit to 230M weekly users, there's no HSA/FSA-native checkout. Whoever builds the compliance layer for AI-driven health commerce captures an enormous payment flow. The same gap exists at every new consumer health front door — DPC practices post-OBBBA, pharma D2C platforms, and cash-pay diagnostic labs.

The common thread: the companies that win aren't asking consumers to change behavior. They're building infrastructure that makes the defined-contribution shift work despite consumer inaction. The same pattern that produced target-date funds and auto-enrollment in retirement is now producing auto-substantiation, auto-routing, and auto-optimization in healthcare.

Additional Reading

- Devenir 2025 Midyear HSA Research Report

- KFF 2025 Employer Health Benefits Survey

- IRS Notice 2026-05 — OBBBA HSA Guidance

- FTC Express Scripts Settlement

- JMCP — GLP-1 1-Year Persistence Data

- EBRI HSA Database — Contribution & Balance Analysis

- OpenAI — Introducing ChatGPT Health

- Amazon Health AI Agent

- ICHRA Enrollment Triples

- SureScripts 2025 Annual Impact Report

- RAND — HDHPs Reduce Utilization Including Preventive Services

- Bronze Plan Popularity Surges in Marketplaces